Definition of Blockchain

A blockchain is an audit trail for a database which

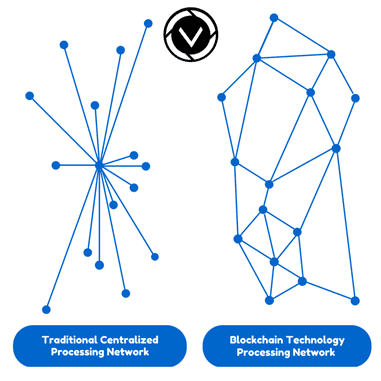

is managed by a network of computers where no single computer is

responsible for storing or maintaining the database, and any computer

may enter or leave this network at any time without jeopardizing the

integrity or availability of the database. Any computer can rebuild the

database from scratch by downloading the blockchain and processing the

audit trail.

Motivation for Blockchain Technology

Traditional databases are maintained

by a single organization, and that organization has complete control of

the database, including the ability to tamper with the stored data, to

censor otherwise valid changes to the data, or to add data fraudulently.

For most use cases, this is not a problem since the organization which

maintains the database does so for its own benefit, and therefore has no

motive to falsify the database’s contents; however, there are other use

cases, such as a financial network, where the data being stored is too

sensitive and the motive to manipulate it is too enticing to allow any

single organization to have total control over the database. Even if it

could be guaranteed that the responsible organization would never enact a

fraudulent change to the database (an assumption which, for many

people, is already too much to ask), there is still the possibility that

a hacker could break in and manipulate the database to their own ends.

The most obvious way to ensure that no

single entity can manipulate the database is to make the database

public, and allow anyone to store a redundant copy of the database. In

this way, everyone can be assured that their copy of the database is

intact, simply by comparing it with everyone else’s. This is sufficient

as long as the database is static; however, if changes must be made to

the database after it has been distributed, a problem of consensus

arises: which of the entities keeping a copy of the database decides

which changes are allowed and what order those changes occurred in? If

any of the entities can make changes at any time, the redundant copies

of the database will quickly get out of sync, and there will be no

consensus as to which copy is correct. If all of the entities agree on a

certain one who makes changes first, and the others all copy from it,

then that one has the power to censor changes it doesn’t like.

Furthermore, if that one entity disappears, the database is stuck until

all of the others can organize to choose a replacement. All of the

entities may agree to take turns making changes and all the others copy

changes from the one whose turn it is, but this opens the question of

who decides who gets a turn when.

How Blockchain Technology Works

Blockchain technology solves these

problems by creating a network of computers (called nodes) which each

store a copy of the database, and a set of rules (called the consensus

protocol) which define the order in which nodes may take turns adding

new changes to the database. In this way, all of the nodes agree as to

the state of the database at any time, and no one node has the power to

falsify the data or to censor changes. The blockchain further requires

that an audit trail of all changes to the database is preserved, which

allows anyone to audit that the database is correct at any time. This

audit trail is composed to the individual changes to the database, which

are called transactions. A group of transactions which were all added

by a single node on its turn is called a block. Each block contains a

reference to the block which preceded it, which establishes an ordering

of the blocks. This is the origin of the term “blockchain”: it is a

chain of blocks, each one containing a link to the previous block and a

list of new transactions since that previous block. When a new node

joins the network, it starts with an empty database, and downloads all

of the blocks, applying the transactions within them to the database, to

fast-forward this database to the same state as all the other nodes

have. In essence, a blockchain establishes the order in which

transactions were applied to the database so that anyone can verify that

the database is accurate by rebuilding it from scratch and verifying

that at no point was any improper change made.

Blockchains in Action

The most obvious example of blockchain technology in use today is Bitcoin.

Bitcoin is a digital currency system which uses a blockchain to keep

track of ownership of the currency. Whenever someone wishes to spend

their bitcoins, they create a transaction which states that they are

sending a certain number of their bitcoins to someone else. Then they

digitally sign this transaction to authorize it, and broadcast it to all

of the nodes in the Bitcoin network. When the next node creates a

block, it will check that the new transaction is valid, and include it

in the new block, which is then propagated to all other nodes in the

network, which adjust their databases to deduct the transferred bitcoins

from the sender and credit them to the recipient.

Blockchain Consensus Protocols

As mentioned above, blockchains are

governed by a set of rules called the consensus protocol. These rules

define which changes are allowed to be made to the database, who may

make them, when they can be made, etc. One of the most important aspects

of the consensus protocol are the rules governing how and when blocks

are added to the chain. This is important because in order for

blockchains to be useful, they must establish an unchangeable timeline

of events, which must be agreed upon by all nodes, so that all nodes can

agree on the current state of the database. Moreover, this timeline

cannot be subject to censorship, thus no single node may be entrusted

with control over what enters it when. There are currently two main

types of consensus protocol: Proof of Work (PoW) and Proof of Stake

(PoS).

Proof of Work is the original

consensus protocol, and is currently used by Bitcoin, Ethereum (as of

January, 2016), and many other blockchains. Proof of Work is based on

puzzles which are difficult to solve, but once solved, it’s easy to

verify that the solution is correct. This is analogous to a jigsaw

puzzle: hours of effort are required to put the puzzle together, but it

takes only a momentary glance to see that one has been assembled

correctly. In Proof of Work consensus, the effort required to solve a

puzzle is called Work, and a solution is called a Proof of Work. In

other words, the fact that I know the solution to the puzzle proves that

someone did the work to find that solution. The solution is proof that

someone did work. Blockchains which use Proof of Work consensus require

such proof for each new block to be added to the chain, thus requiring

Work to be done to create new blocks. This Work is frequently referred

to as ‘mining.’ Proof of Work consensus protocols state that the chain

containing the most blocks is the correct chain because it contains the

most work. Blockchains which use Proof of Work are regarded as secure

timelines because if one node attempted to rewrite history by changing

an old block, its change would invalidate the work on the block it

changed and all blocks after it by making the Proofs incorrect. In order

to convince other nodes that the modified chain is the correct chain,

that node would have to redo all of the work in all of the blocks after

his change to make new, valid Proofs, and because all other nodes are

still making new blocks with new Proofs and adding them to the original

chain, the one node would have to redo all of the old work faster than

all other nodes combined in order to catch up and surpass the original

chain. This is known as a 51% attack, so named because the one node

would have to have at least 51% of the computational power (ability to

do Work and find Proofs) of all nodes combined. If this attack were

successfully carried out, the attacking node would be able to censor

transactions from the blockchain, change the order in which transactions

occurred, or change transactions that node made (but the node would be

unable to change any other node’s transactions).

Proof of Stake is a newer consensus

protocol which was developed to address some perceived weaknesses in

Proof of Work and is currently utilized by Peercoin, BitShares, and

several other blockchains. Some of the advantages of Proof of Stake are

that no Work is required, thus it requires less energy; the 51% attack

is theoretically more expensive; and PoS may encourage a more

decentralized network of nodes than PoW. Proof of Stake consensus

protocols have more varied rules governing which nodes may create new

blocks when than Proof of Work protocols, but in general all PoS

protocols specify that block production is controlled by Stake in the

blockchain rather than computational power. Stake in the blockchain is

balances in the currency the blockchain tracks, thus the greater the

balance a node owns, the more say that node has in block production.

Proponents of Proof of Stake consensus protocols argue that owners of

large amounts of stake will wish to protect their investment and thus

will take action to ensure block production continues smoothly and

securely. Attacks on the network will damage trust in the network,

thereby devaluing the stake. A 51% attack would require the attacker to

buy 51% of the stake in the network, which would be extremely expensive

since the more stake the attacker buys, the higher the price will rise,

and using that stake to attack the network will result in a complete

loss since the value of the stake would be destroyed by the attack. This

is as compared with a 51% attack on a Proof of Work blockchain, which

requires only computing power which typically becomes cheaper when

purchased in bulk, and can be repurposed or sold when the attack is

complete. It is further supposed that, whereas Proof of Work consensus

incentivizes greater centralization because computing power is cheaper

with centralized cooling and power, no such incentive exists with Proof

of Stake since a typical smartphone has more than sufficient

computational power to produce blocks for a PoS blockchain.

Blockchain Technology and Online Voting

Another application for blockchain

technology is voting. By casting votes as transactions, we can create a

blockchain which keeps track of the tallies of the votes. This way,

everyone can agree on the final count because they can count the votes

themselves, and because of the blockchain audit trail, they can verify

that no votes were changed or removed, and no illegitimate votes were

added.

Comments

Post a Comment